Is it necessary to regulate credit rating agencies?

Karminsky A.1

1 National Research University Higher School of Economics, Moscow State Institute of International Relations (University)

Статья в журнале

Global Markets and Financial Engineering ()

Цитировать:

Karminsky A. Is it necessary to regulate credit rating agencies? // Global Markets and Financial Engineering. – 2014. – Том . – № . – С. 21-30. – doi: 10.18334/gmfe.1.1.274.

Аннотация:

Rating scores have acquired the status of one of the key informative tools in the financial sector. At the same time it is impossible to confirm the reliability of each score. It is the opinion of a rating agency with respect to a certain aspect of one company’s or one bank’s activity, such as, for example, subjects of evaluation of a business solvency. Goodwill is a natural control. But is that enough? And how can one compare the assessments of different agencies?

This article presents methods that answer these and related questions of regulators, issuers and investors. The emphasis is on the remote approach that has passed through a specific practical approbation.

Ключевые слова: rating, rating agency, scale correlation, regulator

Introduction

A rating is a comprehensive assessment of risk. Adoption of the Basel recommendations (Basel II and Basel III) has enabled expanded rating use in the XXI century. Ratings simplify assessment of business partners for companies, allow savings for investors and issuers, and promote development of a country’s financial control.

Credit ratings are comprised of independent evaluations:

· Financial condition of companies, banks, financial instruments needed for the formation of a contemporary business environment;

· Business solvency (credit risk) of business partners;

· Accreditation possibilities (access to certain products or services) As a result of a comprehensive evaluation of a large amount of information provided by the issuing company (in the event this rating is requested, a contact rating) or public information about a company (in the event this rating is not requested, a remote rating), the agency issues its opinion about creditworthiness, financial stability, reliability and/or competitiveness of a company [2, 3]. This is exactly what a rating feature is all about-in the ability to convert a large amount of information and certain number indicators

of a company into one assessment on a unified scale [9,10].

Ratings are necessary for all of the participants of economic relations, whether it is an issuing company, which presents an inquiry for a rating, borrowers of this company, investors or a regulatory authority. First, the presence of a rating value increases the value of the company and thus attracts investors. Secondly, the presence of the rating value itself increases the status of the company in the eyes of its customers and credit institutions with which the company collaborates. Another positive feature of a credit rating value is that the company that orders the evaluation from a certain rating agency sees increased references in the media.

For a regulating authority, credit ratings serve as a unique license for a company’s admissibility into certain transactions, including securities auctions, corporate bonds listing to be included in the quotation list on the stock exchange and others. Ratings simplify the process of monitoring companies and identifying situations that require, in case of problematic situations, bailouts or bankruptcy.

Ratings present interest not only for business-structures, but for governmental regulating authorities as well. Restrictions on the effective rating use are comprised that [4, 7, 8, 11]:

· there is a relatively small number of actualized contact ratings;

· difficulties are observed in comparing ratings by different rating agencies;

· a synergetic effect on the availability of competitive assessments is absent;

· there is a need in the increased use of independent rating assessments, primarily due to simulation capabilities;

· there is a necessity for continuous improvement of risk assessment methodology, including a methodology, based on the application of contemporary mathematical models.

Management solutions production system includes a pyramid, which is based on both expert and model components. Model development is oriented towards:

· reducing the load for the regulator through the use of model components;

· using integrated informative solutions in the expert community;

· additional single-pointed expert solutions, including expert review of each specific situation.

Increased use of independent rating agencies in assessing credit risks [1] has been occurring recently, as well as rating models and possibility of bank defaults. Largest commercial banks give considerable attention to building a system of model ratings, based on a concept of a single rating domain, including within the IRB-approach [13]. Ability to access the ratings by using models is provided to the regulatory authority, as well as to commercial banks, followed by presentation of results to the regulator and customers.

Increased demand for rating services leads to the upsurge in the number of credit rating agencies. However, due to the nonexistence of a single standard of issuer ratings, risk assessment becomes more complicated [15, 4]. Several large companies and banks self-dependently analyze their business partners. Thus, several obvious questions are raised:

· Is it necessary to regulate rating use and rating activity as such?

· How to compare internal assessment ratings, made by bank and company analysts, with rating agency rating valuation?

· Is it possible, in general, to compare rating assessments and, as an appropriate tool, rating scales?

Recently, a variety of relevant research studies have been implemented, with a major emphasis on the domestic topics [5, 6, 12, 14], as well as a corresponding testing methodologies appraisal has been developed under the expert council of the Ministry of Finance. In conjunction with mega regulator occurrence in Russia, above mentioned questions have intensified, and require custom reasoning. This is what this publication is geared towards.

Accumulated experience of rating scale comparison

A rating scale comparison mechanism is indispensable for all economic relations participants, including a borrower and a regulator. However, most sources are directed at identifying differences in issuer estimates by various agencies and analyzing roots of a rating mismatch. Most often, rating comparison is handled in pairs [13].

All rating agencies (RA’s) practically use identical letter scales with negligible differences. The probability of default is the basis of ratings, though different agencies define default differently. All agencies estimate relative risk, and not absolute risk- that is, issuers are ranked according to a rating scale, and do not openly estimate default probability of a particular issuer. Furthermore, a rating agency is not required to use probability of default as a risk measure. Moody’s uses this index as an expected loss in case of default. Russian agency “Rus-Rating” applies both indicators. Therefore, notwithstanding rating agencies equally evaluating default probability of an issuer-company, their rating estimates may differ from each other.

Another important criterion in rating estimate differences is that agencies use different methodology. For instance, international rating agencies assess default risk of an issuing company in the long term, and use methodology called “through-the-cycle”. Essentially, they assess a company’s stability for the following 3-5 years. However, this methodology boasts a significant drawback; any significant company event, which happens during the above mentioned time, will not be accompanied by a timely rating agency’s reaction. In return, Russian rating agencies primarily use “point-in-time” methodology. It reflects rating agency’s opinion on an issuing-company’s creditworthiness at a specific point in time.

By no means, another unimportant reason for differentiating rating agency estimates, is that international rating agencies are able to use both domestic and international scales, but Russian agencies, in turn, only use the national scale. Thus, Russian rating agencies rank issuers against the best Russian borrower, which is assigned a highest creditworthiness rating. International agencies evaluate issuers on a national scale in the same way, but international scale is limited atop by the country ceiling- the level of an independent rating of the Russian Federation.

In addition to all the above reasons, rating agencies can use a multitude of factors to determine the credit rating of an issuer. Both quantitative and qualitative factors may vary, along with internal and external differences.

For these reasons, multiple comparison of rating scales presents to be a very currently pending question. In Russian practice this contributes to the formation of a Common rating range – adopting a basic scale and forming an external and internal ratings mapping system into a benchmark to be applied to every rating class member [15].

Scale comparison methodology of rating agencies includes [6, 14]:

· Scale rating mapping methodology;

· Principles and criteria for rating scale correlation;

· Correlation scale models, including an econometric model

· Mapping Table audit and coordination of its structure.

The rating agencies compared in the frames of this work include major rating service market participants, both domestic (AK&M, HPA, “Rus-Rating”, “Expert PA”), and foreign ((Fitch, Moody’s and S&P) using national and international scales.

Currently, one can highlight three main rating scale comparison methods: remote [6, 14], econometric [12] and nonparametric [5]. In this paper, we will use the most popular one-the remote method.

Remote rating scale comparison method

For rating activity regulation it is important to have an opportunity to compare rating estimates of different agencies and to identify systematic inconsistencies between them, particularly with regard to regulating the subjects of rating. A solution remedy for the stated problem is the possibility to compare rating scales of different agencies and to present evaluation results in a single scale, by monitoring agency’s activities, rating principle method correlations and nonexistence of rating tampering. For these purposes, this paper will use remote method, which is based on minimizing the integral intervals between estimates in a single scale.

Rating scale comparison methodology that can be used to identify correlation between ratings assigned to Russian companies is offered to compare bank rating scales as well [14, 4].

In accordance with the remote approach, the benchmark scale is chosen first. It is natural to select a benchmark scale from one of the international rating agencies. In the quoted works, Moody’s rating scale was chosen. Review demonstrates a practical result invariance from the choice of a scale, if this scale is sufficiently standardized. Hereafter, all scales are shifted from letter notations into numerical scales.

In accordance with the methodology, we find the transformed image of different agency scales and the benchmark scale so that the optimality criterion is executed. Consequently, the purpose of the next step is to find the optimal functions Fi , which reflect an i-th scale into the basis for all agencies, i=1 … , N. Integral closeness measure between a pairwise compatible estimates of the same subject should be minimal.

Work [14] used the minimization of the sum of a squared difference method

where i-is the scale, j-is the subject, t – is the analyzed moment of time, Rijt -rating estimate. All these parameters represent Q, which is being summarized. In addition, various functional dependencies Fi have been examined, and it was concluded that most accurately this functional connection is described with a power function.

To solve the problem of extremes, econometric package possibilities were used, because criterion (1) is a quadratic form, extremum of which can be found by solving a system of linear equations.

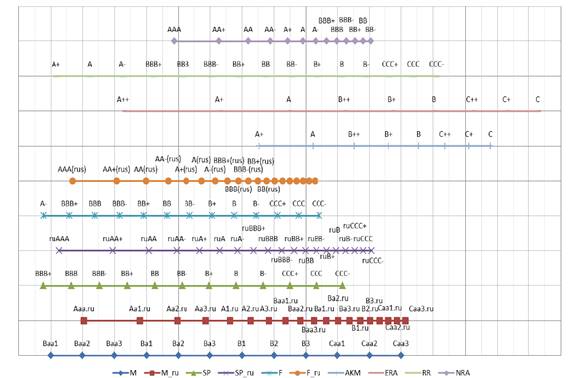

Comparison results obtained from the data for the previous 5 years (2006-2010 years) can be represented graphically (Fig.1) or in a tabular format (Table 1, 2010 data mapping including correlation rounding’s). Based on this, correlation is formed between the scales, which can be used not only for regulatory purposes, but for risk-management in banks as well. It should be noted that the resulted correlation between international ratings somewhat differs from agreements that are traditionally used in practice.

Figure 1. Chart of correlation between rating agency scales that work in Russia

(source – compiled by author)

It should be noted, that results presented in the chart, are sufficiently stable, which indicates the absence of significant rating tampering. Herewith, results with various basic scales, comparison methods and eligibility criteria scales were compared.

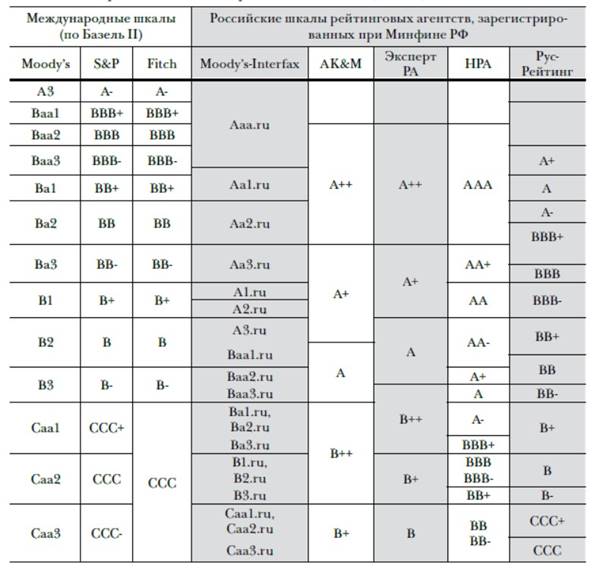

Table 1. Rating scale correlation of the Russian Banks (2010)

(source – compiled by author)

Conclusion

Credit ratings present a highly demanded estimation tool, as well as rating agency’s opinion on the debtor’s ability to meet its financial obligations. Due to the growth of the rating industry, a question of regulating their activities comes to the forefront, which can also serve as a comparison of rating scales for different classes of issuers.

By giving different names to their estimates, rating agencies, in fact, assess similar concepts. However, evaluation methods and approaches often differ. Most efforts are directed at pairwise comparison ratings. The majority of researchers, at that, do not try to correlate the rating scale, but search for differences in rating assessments and the reasons for these discrepancies.

The proposed remote method is based on the multitude correlations of rating scales and uses the features of econometric software packages. Given the lack of correlating rating scale experience for financial and industrial companies, as well as the need for regular updating of correlation results, the subsequent empirical analysis is relevant and is of practical interest.

Страница обновлена: 22.01.2024 в 18:47:14